English

English Chinese

ChineseScan QRCode

Although the auto market has shown signs of rebound on a month-on-month basis, the latest auto market forecast released by the China association of automobile manufacturers for 2020 is still "down by 15%-25% year on year". In the shrinking living space, "head" enterprises occupy the favorable terrain, waiting for work, waiting for the opportunity to move; The "middle class" car companies, whose volume is in the range of 500,000 to 800,000 vehicles, are likely to rise or fall in the new round of competition. On the one hand, the middle tour car enterprises, including chery, byd, dongfeng Honda, gac Honda, faw Toyota, gac Toyota, etc., give full play to their expertise and gain a number of loyal fans. On the other hand, the rising space is occupied by the "head" enterprise of "two million vehicles, one million vehicles", and if it is not careful, it will encounter the risk of "getting out". Shenlong automobile is a case in point.

Since 2018, the growth rate of China's automobile market has shown a downward trend, and the market has entered a period of reshuffle. The "Matthew effect" has become more obvious, and the advantages of enterprises with brand power and product premium power have become more obvious. The covid-19 outbreak at the beginning of 2020 is both a "catalyst" and a "mirror of evil", reflecting the current market landscape. Will this become the "norm" in the future, or a "prelude" to a new landscape?

Based on this, the economic daily-china economic net automobile channel will launch a series of reports, from the historical evolution, current performance, product layout and structure, brand power and marketing power and other dimensions, to analyze the possible causes and consequences of the new pattern. Can 2020 be the origin of reshaping the domestic automobile industry pattern? Today launched the sixth - high or down "middle" car companies have a hard time.

Every family has its own difficulties. In the domestic auto market, for the auto companies with annual production and sales of "middle class" (volume between 500,000 and 800,000 units), survival and development are the "keywords". Although the market had rebounded from signs, RGL association's latest car market is expected in 2020, is still "fell by 15% - 25%", in diminishing the survival space, "head" enterprises occupy the favorable terrain, earlier and, the waiting game, "middle" automakers are likely in the new round of competition high or fall back.

According to the China association of automobile manufacturers, China's auto market both saw year-on-year growth in production and sales in April, up 2.3 and 4.4 percentage points respectively. The data of the passenger car market joint meeting also showed that China's car market, under the influence of several favorable factors, has promoted the "v-shaped" reversal trend. In April, the sales volume of passenger cars in the narrow sense reached 1429,067 units, with a month-on-month growth of 36.6% and a year-on-year decline of 5.6%, and the growth rate was the second highest in nearly 20 months.

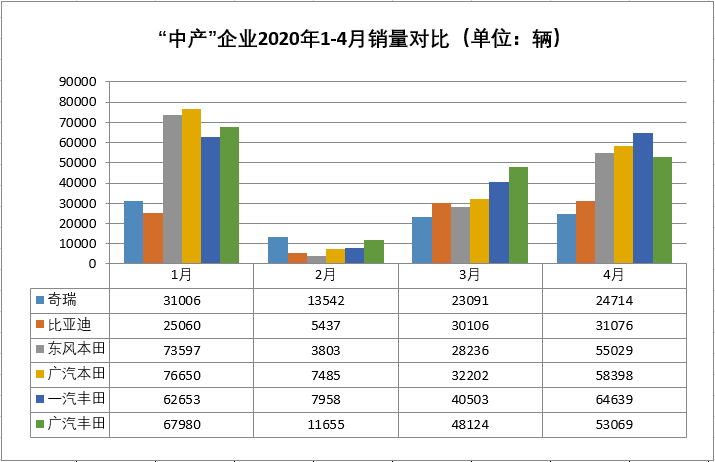

According to the sales data in recent years, chery, byd, dongfeng Honda, gac Honda, faw Toyota and gac Toyota are just in the "middle class" stage of enterprise development. From January to April this year, the cumulative sales of chery and byd were 92,353 and 91,679 units, respectively, down 24.40% and 39.76% from the same period last year, which were greatly affected by the epidemic. The joint venture between Toyota and Honda has performed well under pressure as a whole, especially Toyota of guangzhou automobile, with the highest cumulative sales of 180,828 vehicles, down only 10.96% year on year.

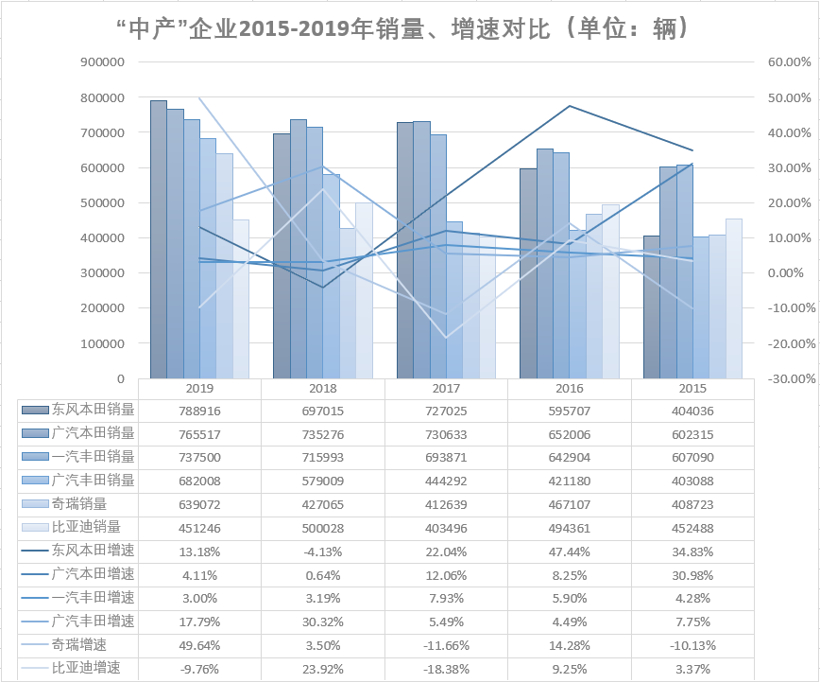

An overview of the market performance in the last five years (2015-2019) shows that chery has risen steadily, byd has fallen, and the joint venture between Toyota and Honda has grown significantly. Among them, after several years of low energy consumption, chery broke out against the trend in 2019, with a total wholesale sales volume of 605,600 units, up 12.1% year on year. As for byd, its sales volume has fluctuated significantly in the past five years, from a peak of 27.09% year-on-year growth in 2018 to a 13.34% year-on-year decline in 2019, leaving it out of the "middle class" of 500,000 vehicles.

Among the joint venture brands, the growth rate of dongfeng Honda, gac Honda and faw Toyota has gradually slowed down in the past five years, from 34.83%, 30.98% and 4.28% in 2015 to 13.18%, 4.11% and 3.00% in 2019, respectively. The sales volume has reached an annual average of 700,000 to 800,000 vehicles in 2019. Gac Toyota, which had been developing slowly before, rose rapidly in 2018 and 2019, with a growth rate of 30.32% and 17.79% respectively, showing the most prominent growth trend.

In recent years, Toyota and Honda have started to implement the "two-car strategy", which is largely based on the growth experience of Volkswagen in China. The core technologies of the corresponding models of the "two-car strategy" are roughly the same. On the one hand, the product structure is rapidly expanded to increase the market share and reduce the supporting costs. On the other hand, they are also faced with the risk of product failure, such as the "engine oil gate" incident of Honda L15B engine in early 2018 and the "engine oil gate" incident of Toyota 2.5l hybrid not long ago. These are common problems encountered in the process of "two-car strategy".

In contrast, there is no multinational car companies technology "endorsement" of the independent brand, more rely on their own development, and strive to find a unique way. After years of research and development, chery has become the only independent brand to realize "three major pieces of self-research", which can endure loneliness and will eventually receive "flowers and applause". Taking the electric as the breakthrough point, while gradually weakening the fuel cars, byd has gradually enriched the new generation of "dynasty series" products, and won the favor of international giants such as Toyota and mercedes-benz by virtue of its efforts in the core technologies of "three electric", and won the equal communication between its own brands and multinational automobile enterprises.

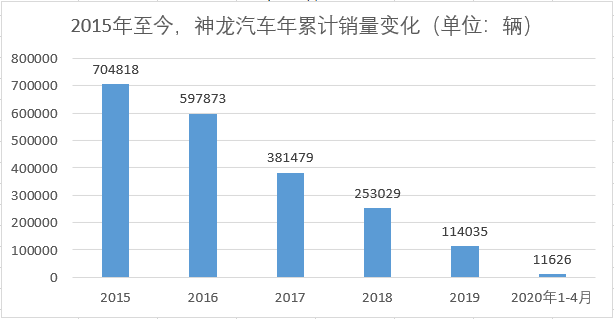

Standing between the "middle class" echelon, opportunities and risks coexist. On the one hand, I will give full play to my expertise, gain a group of loyal supporters, and seek quantity and quality. On the other hand, the upward space is occupied by "head" enterprises with "two million or one million vehicles". If they are not careful, they will be "out of the picture" : from the peak of production and sales of 700,000 vehicles to the low of more than 100,000 vehicles, the transformation of shenlong automobile in the past five years is enough to become a "middle class" automobile company.

AMS2024 Exhibition Guide | Comprehensive Exhibition Guide, Don't Miss the Exciting Events Online and Offline

Notice on Holding the Rui'an Promotion Conference for the 2025 China (Rui'an) International Automobile and Motorcycle Parts Exhibition

On September 5th, we invite you to join us at the Wenzhou Auto Parts Exhibition on a journey to trace the origin of the Auto Parts City, as per the invitation from the purchaser!

Hot Booking | AAPEX 2024- Professional Exhibition Channel for Entering the North American Auto Parts Market

The wind is just right, Qianchuan Hui! Looking forward to working with you at the 2024 Wenzhou Auto Parts Exhibition and composing a new chapter!

Live up to Shaohua | Wenzhou Auto Parts Exhibition, these wonderful moments are worth remembering!

Free support line!

Email Support!

Working Days/Hours!

Copyright © 2018, PKT Auto Parts All Rights Reserved

浙ICP备18033565号-1

浙公网安备33038102332475号

浙公网安备33038102332475号