English

English Chinese

ChineseScan QRCode

Decades ago, German cars helped China to initially establish the foundation of the modern automobile industry and market through joint ventures. Both Chinese and foreign countries were unexpected. Today's former students finally taught their teachers a lesson. In the last week of February, a special plane for German ChancellorMertz landed in Beijing. Together with him are the leaders of three auto giants, VW, BMW and Mercedes, as well as about 30 top business leaders in Germany. This was his first visit to China after taking office as prime minister, and the delegation lineup almost covered all the essence of German industry.

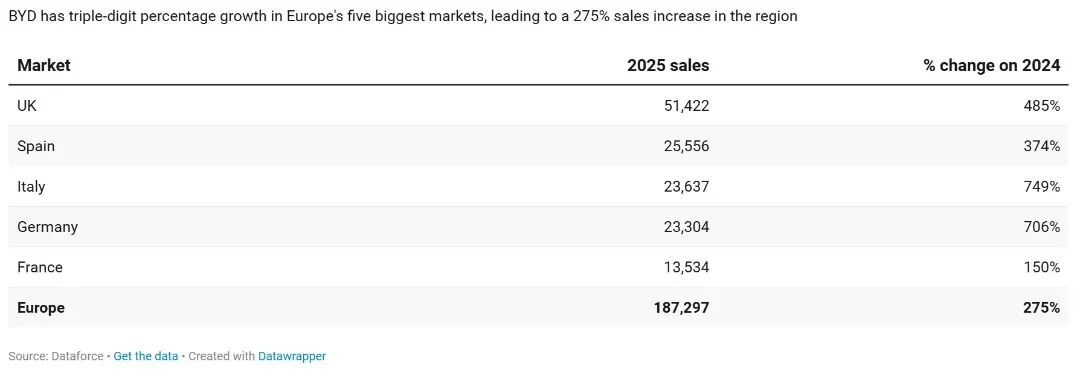

Both sets of data are relevant for at least some of the purposes of Mertz. One group is the data released by the German Economic Research Institute. In 2025, German automobile exports to China fell below 14 billion euros, compared with nearly 30 billion euros three years ago. The other group is Dataforce's data. In January this year, sales of Chinese auto brands in Europe grew 80% year-on-year, with a market share of 7.4%, almost double that of a year ago. However, European automobile companies are taking over the obsolete plug-in and hybrid market led by BYD. This also makes BYD overtake MG and become the most popular Chinese auto brand in Germany.

For a time, plug-in hybrid has been regarded as a transitional and marginal technical route overseas, but it has become a technical trend for Chinese automobiles to export overseas. Mertz hopes to reshape the pattern of Sino-German automobile industry, but the Chinese automobile industry should go beyond the gains and losses of the single market and have a deep understanding of the underlying law and logic of the industry.

GAC MOTOR GAC MOTOR GAC MOTOR GAC MOTOR REVERSE

The decline in German auto exports to China is not a short-term fluctuation. This trend has been in place for three years, from a peak in 2022 to a downward trend in 2025. German auto and parts exports fell below 14 billion euros last year, from close to 30 billion euros three years ago, according to the German Institute for Economics. As the most important overseas market in Germany, the demand structure of Chinese market is changing. On the one hand, the product power of Chinese local brands in the new energy field is rapidly increased, directly squeezing the market share of German cars.

On the other hand, the preference of Chinese consumers for intelligent automobile also challenges the product definition of German automobile enterprises. Mercedes-Benz China CEO Dong Oufu said frankly this month: "All fields are facing price wars and new entrants, and the market structure changes dramatically." Meanwhile, Chinese brands are opening up in Europe. In January, against the backdrop of a 3.6% decline in the overall European market, the sales volume of Chinese brands increased 80% to 70465 units, and the market share increased from 4.0% a year ago to 7.4%. SAIC MG took the top place with the sales volume of 18537 vehicles, but the decline of 3.8% significantly narrowed the leading edge. MG ZS small SUV sales plummeted by 20%, directly affecting overall performance. BYD sold 17630 units in January, a year-on-year increase of 173%, and exceeded MG for the first time in the German market with the registered number of 2069 units, a year-on-year increase of 1000%.

Ras Bearkovsky, head of BYD Germany, said the goal was to make Germany the benchmark market of BYD in Europe. Chery is the fastest growing Chinese brand, with sales of 17106 units in January, a year-on-year increase of 354%. Through the combination of Jaecoo, Oumengda and other sub-brands, Chery is trying to cover more market segments. Chinese brands form a relatively centralized competition pattern in Europe. The GEELY Group ranked fourth with 5079 units and fifth with 4249 units at ZERO, a 409% increase in the latter also deserves attention. This trend of declining and declining forms an important background for the visit of Mertz. Before leaving, he said that fair and transparent trade is the prerequisite for the success of the Germany - China relationship, and it is necessary to discuss how to solve the impact of "systematic overcapacity, export restrictions and market access barriers" on competition. This speech was meant for both China and the German automobile industry.

Insertion and mixing breaking bureau: accurate introduction of technical routePlug-in hybrids have played a key role in this round of growth. In January, the proportion of Chinese brands in European sales rose to 29% from 11% in the same period last year. However, in the whole European market, the plug and mix sales in January increased by 32% year-on-year, higher than that of pure electricity by 14%. BYD is a typical example of this trend. Last year, Seal U (corresponding to Song Plus in China) became the most popular plug-in hybrid model in Europe with 79518 units, with sales growth of nearly 600%.

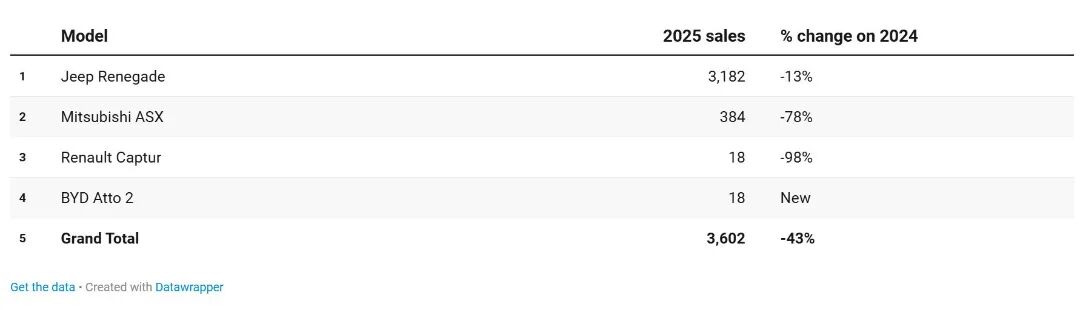

In January of this year, Seal U sales increased by 178% to 7390 units, ranking among the top in the mid size SUV segment, second only to Skoda Kodiaq. The success of this model proves that European consumers do not necessarily need plug-in hybrids, but rather truly useful plug-in hybrids. More strategically significant is the small SUV market. According to Dataforce data, the total sales of small SUV segments exceeded 2.24 million units last year, but plug-in hybrid models only accounted for 3602 units, accounting for 0.16%. After the discontinuation of Jeep Renegade PHEV and Renault Captur PHEV, this niche market has almost become blank. BYD plans to fill this gap with Atto 2 PHEV (domestic counterpart UP). This model is equipped with an 18 kWh battery, with a WLTP pure electric range of about 90 kilometers and a comprehensive range of over 1000 kilometers. In the German market, the official starting price of Atto 2 Boost version is 38990 euros. After adding BYD's 11500 euros manufacturer subsidy and the German government's approximately 4500 euros electric vehicle subsidy, the actual price drops to 22990 euros. Meanwhile, hybrid models such as Toyota Yaris Cross and Volkswagen T-Roc in the same class have a starting price of over 35000 euros. However, the price of Atto 2 is about RMB 186000, which is still more than double the starting price of over 70000 yuan for domestic distributors. Florian Ulbrich, the product manager of BYD Germany, provided a data: only 2% of Germans drive over 100 kilometers per day. This means that a pure electric range of 90 kilometers can meet the daily commuting needs of most people. For most people in Germany, a range of 90 kilometers allows them to drive in pure electric mode for most of the time, "he said.

This product definition based on user scenarios is one aspect of enhancing the competitiveness of Chinese car companies. Another product that has performed well is the Dolphin Surf, which contributed 3007 units in the micro electric vehicle segment in January, ranking third only to Renault R5 E-Tech and Citroen eC3. From Seagull to Yuan UP and then to Song Plus, BYD's product line has covered about 90% of the segmented areas in the European market. The mixed use strategy also takes into account tariff considerations. At present, the EU imposes a 27% tariff on Chinese pure electric vehicles, while the tariff on plug-in hybrid models is only 10%. Before the full release of production capacity in the Hungarian factory (where the Seagull and Atto 2 pure electric versions are about to be put into production), plug-in hybrid models play a role in reducing the impact of trade barriers.

03 cycle dilemma: catching up and challenges for German car companiesFaced with competition from Chinese brands, German companies are not without countermeasures. In terms of localized research and development, Volkswagen, BMW, and Mercedes Benz all have mature research and development centers in China, and these institutions are transforming from "adapting to the Chinese market" to "participating in global research and development". The technological cooperation between Volkswagen and Xiaopeng Motors, as well as the joint venture established with Horizon Robotics, are all manifestations of this trend. In 2023, Volkswagen will invest approximately $700 million in Xiaopeng, and the two parties plan to jointly develop two Volkswagen brand electric vehicle models. The joint venture between BMW and Chengmai Technology is also strengthening its local research and development capabilities in the field of intelligent cockpits.

In terms of technological roadmap, German car companies are also adjusting. Mercedes Benz has announced an increase in investment in hybrid models, while BMW continues to optimize its plug-in hybrid products while maintaining its pure electric route. These adjustments indicate that German companies are re evaluating the technological trends in the Chinese market and trying to keep up with the pace. At the supply chain level, CATL and EVE Energy have established factories in Germany to provide battery support for European car companies; Huawei's intelligent driving solution is also in contact with some European brands. This technology procurement and cooperation can help European car companies shorten their catch-up cycle in the field of electrification. However, the decision-making cycle of German car companies is relatively long. A new car model usually takes 3-5 years from project approval to mass production, while the iteration speed of Chinese car companies has been compressed to about 18 months. This difference in rhythm means that German companies find it difficult to keep pace with Chinese brands in the short term. Even if we make up for our shortcomings through technology procurement and collaborative research and development, the adjustment of organizational structure and the transformation of thinking patterns still require time. One of the core demands of M ö tz's visit to China this time is to buy adjustment time for the German automotive industry. The German Association of Automobile Manufacturers had previously called on the Chancellor to initiate consultations on relevant issues.

But from a practical perspective, the space that Germany can strive for is limited. The advantages of China's new energy vehicle industry chain have been formed and will not change in the short term due to external pressures. A more realistic path is to stabilize expectations through dialogue, ensuring that German companies can still gain development space in the Chinese market, while filling the gaps through localized research and development and technology procurement. During his trip, Mertz will visit Mercedes Benz electric vehicle factories and Siemens energy facilities, both of which send a signal that German companies are still investing heavily in China and the interests of both sides have not been severed. From a longer-term perspective, the interaction between the Chinese and European automotive industries is shifting from one-way technology transfer to two-way technology flow. German companies absorb China's experience in intelligence through localized research and development, while Chinese companies use the European market to verify their product definition capabilities. This interaction itself helps promote technological progress. But at the moment of cycle transition, the adjustment of offensive and defensive momentum has just begun.

AMS2024 Exhibition Guide | Comprehensive Exhibition Guide, Don't Miss the Exciting Events Online and Offline

Notice on Holding the Rui'an Promotion Conference for the 2025 China (Rui'an) International Automobile and Motorcycle Parts Exhibition

On September 5th, we invite you to join us at the Wenzhou Auto Parts Exhibition on a journey to trace the origin of the Auto Parts City, as per the invitation from the purchaser!

Hot Booking | AAPEX 2024- Professional Exhibition Channel for Entering the North American Auto Parts Market

The wind is just right, Qianchuan Hui! Looking forward to working with you at the 2024 Wenzhou Auto Parts Exhibition and composing a new chapter!

Live up to Shaohua | Wenzhou Auto Parts Exhibition, these wonderful moments are worth remembering!

Free support line!

Email Support!

Working Days/Hours!

Copyright © 2018, PKT Auto Parts All Rights Reserved

浙ICP备18033565号-1

浙公网安备33038102332475号

浙公网安备33038102332475号