This article is reproduced from Gasgoo Information. A few days ago, some media quoted industry sources as saying that the quotation of Lithium Iron Phosphate (LFP) batteries of CATL will increase by 10% to reflect the increase in raw material costs. In response to the news, Ningde Times immediately responded: the news is not true.

In the face of the above response, many people who eat melon on the Internet have left messages saying: "There is no wind and no waves"; "It must rise, but it is strange if the supply exceeds demand." What is more, "the increase of 10% is not true, but it is actually an increase of more than 10%."

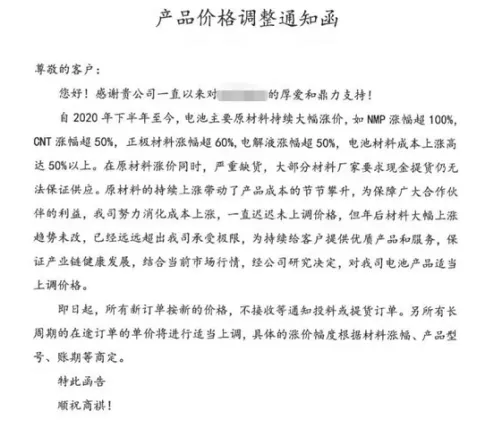

Picture source: Ningde Times

Lithium material prices remain high and may reach new highs in the second half of the year

As we all know, the Ningde era denies the rumors of price increases because of the rising prices of upstream raw materials for lithium batteries.

Since 2020, the price of upstream raw materials for lithium batteries has been maintained at a high level. Data show that as of May 18, the price of battery-grade lithium carbonate has risen from last year’s “low” price of 38,000 yuan/ton to the current 89,000 yuan/ton (average price), an increase of 134%; lithium hydroxide has increased from 60,000 yuan/ton rose to 87,500 yuan/ton (average price).

According to analysis by industry insiders, the continuous increase in the price of lithium-related battery materials is driven by the strong demand for downstream new energy vehicle power batteries; on the other hand, it is also subject to the current tight supply and demand of lithium materials.

According to the latest statistics of the China Automobile Association, the cumulative sales of domestic new energy vehicles from January to April this year was 732,000, a year-on-year increase of 249.2%, which led to a year-on-year increase of approximately 241% in the installed capacity of power batteries; another data from SNE Research It shows that the installed capacity of power batteries in overseas markets increased by 96% year-on-year in the first quarter.

In the next five years, as the number of new energy vehicles continues to grow rapidly, relevant agencies estimate that the global penetration rate of new energy vehicles is expected to reach 20% in 2025, and their sales will exceed 18 million. At the same time, considering other lithium carbonate application scenarios such as energy storage, 3C consumer electronics, and traditional industries, it is estimated that the global demand for lithium carbonate will reach 1.24 million tons in 2025, 3.6 times that of 2020.

On the one hand, the demand for raw materials continues to rise, and on the other hand, it is the insufficient supply from the supply side. It is reported that Australia, Chile, Argentina and other countries are the world's major lithium mine exporters, but in the past year, due to the impact of the new crown pneumonia epidemic, the expansion plans of lithium mining giants including SQM and Livent have slowed down. In the past week, due to the aggravation of the epidemic, Chile, as one of the world’s major exporters of lithium mines, announced that it will adopt stricter epidemic prevention measures from the second quarter. This has also led to industry concerns about the tight supply of power battery raw materials. Intensified further.

From the perspective of the industry, due to the imbalance between supply and demand, the price of lithium materials may continue to rise in the future, or even reach new highs. At the "New Energy Battery Material Frontier Technology and Intelligent Manufacturing Summit Forum" held recently, Xu Aidong, secretary general of the China Nonferrous Metals Industry Association Cobalt Industry Branch, pointed out that the current round of lithium industry demand cycle is strong, but it is limited by the global supply-side lithium resources and Lithium smelting does not match each other, and the time for lithium prices to remain high is expected to exceed expectations. In the second half of this year, the price of battery-grade lithium carbonate is expected to rise to 100,000-120,000/ton, and the lithium price center is expected to be 90,000-100,000/ton within 3 years.

Power battery companies are under pressure to move forward, and the industry reshuffle is intensified

Faced with the sharp increase in raw material prices due to tight supply and demand, power battery companies are obviously under pressure, so that when the Ningde era responded to the price increase as false news, netizens made the above ridicule.

Indeed, since the prices of raw materials have been rising, some battery manufacturers have fallen into a dilemma: on the one hand, if they increase battery prices, they may lose long-term orders; on the other hand, if they do not increase prices, companies will be under significant pressure. Survival may be threatened.

The actual situation is that, in the face of the pressure transmitted by the upstream raw material prices, the power battery suppliers of the first echelon (such as the Ningde era) have not yet raised the price of battery loading, and the second and third echelon companies have to be forced to increase. price.

Picture source: network screenshot

It is understood that since the beginning of this year, companies such as Far East Battery, Zhuoneng New Energy, Penghui Energy, Hengdian Dongci and Delangen have issued battery price increase letters. A person in charge of a battery company said frankly, "This situation is very rare. If it is not a last resort, the company is unwilling to increase the price. If it does not increase as much as possible, the price increase may lose customers."

As a leading domestic power battery company, Chairman of CATL, Zeng Yuqun, also made a statement on the rise of raw materials at the recent shareholders meeting: "If the raw materials rise very high, it will definitely have a greater impact on our costs. But high. We are also considering this issue to the extent to which it will be passed on to the downstream." He also put aside the "ruthlessness", "If prices are increased desperately, they will have a little frustration, because we can exclude it."

Zeng Yuqun also added, “Lithium carbonate or nickel and cobalt, the whole world is just that. Now we are also doing some layouts for nickel, cobalt and lithium, so that they can really understand that it is a reasonable price (business) to achieve long-term development.”

Although battery companies have not followed the trend to increase prices, the impact of rising raw material prices on all companies cannot be ignored, especially the decline in gross profit margin. Therefore, in the face of rising raw material prices and declining gross profit, cost reduction has become an important part of battery companies to improve their market competitiveness.

Picture source: Ningde Times

In response to the pressure on the cost side caused by the increase in the price of major materials this year, Ningde Times stated that it mainly reduces production costs and raw material costs by improving product performance and energy density, optimizing product design, improving product yield, and reaching in-depth cooperation with the industry chain. . In addition, CATL is constantly improving its manufacturing and management levels, implementing intelligent manufacturing internally, improving production processes, increasing product yields, and reducing costs.

Penghui Energy stated that the impact of the price increase of raw materials will be resolved from two aspects to maintain a reasonable gross profit margin: The first is to reduce costs, rely on R&D and technological progress to increase battery capacity, energy density, and optimize formula structure. Etc., to reduce unit ampere-hour or watt-hour costs; to reduce labor costs by improving equipment automation; to reduce manufacturing costs by refined management, lean manufacturing, internal tapping of potential, optimization of process flow, and reduction of defective rates, and so on. The second is the transmission of battery prices. Through battery price increases, downstream customers share the pressure of price increases. In fact, some battery products have already increased prices.

However, it needs to be pointed out that, unlike head battery companies, for small battery companies, raw material prices and declining gross profit margins will further compress their living space. It is foreseeable that the reshuffle of the power battery industry will be further intensified. Relevant data shows that in recent years, the number of domestic power battery suppliers has been showing a downward trend year by year, from about 130 in 2016 to about 70 in 2020. At the same time, the market concentration of the industry has also increased significantly. The installed capacity ranks TOP5 companies, and its market share has further increased from 85% in 2016 to 94% in 2020.

AMS2024 Exhibition Guide | Comprehensive Exhibition Guide, Don't Miss the Exciting Events Online and Offline

Notice on Holding the Rui'an Promotion Conference for the 2025 China (Rui'an) International Automobile and Motorcycle Parts Exhibition

On September 5th, we invite you to join us at the Wenzhou Auto Parts Exhibition on a journey to trace the origin of the Auto Parts City, as per the invitation from the purchaser!

Hot Booking | AAPEX 2024- Professional Exhibition Channel for Entering the North American Auto Parts Market

The wind is just right, Qianchuan Hui! Looking forward to working with you at the 2024 Wenzhou Auto Parts Exhibition and composing a new chapter!

Live up to Shaohua | Wenzhou Auto Parts Exhibition, these wonderful moments are worth remembering!

Free support line!

Email Support!

Working Days/Hours!

Copyright © 2018, PKT Auto Parts All Rights Reserved

浙ICP备18033565号-1

浙公网安备33038102332475号

浙公网安备33038102332475号

English

English Chinese

Chinese