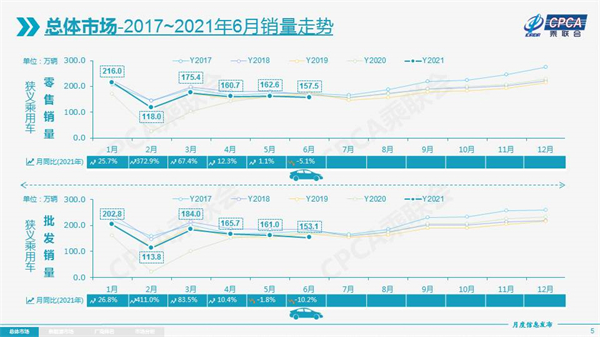

On July 8, the Passenger Car Market Information Joint Conference released data showing that in June, the domestic narrow passenger car sales totaled 1.575 million, a year-on-year decrease of 5.1%; compared to when the "National Five" inventory was cleared in June 2019 The peak sales of the company dropped by 11%. In the first half of the year, domestic sales of narrow passenger vehicles totaled 9.942 million units, a year-on-year increase of 28.9%, setting a new growth rate since 2011.

In this regard, Cui Dongshu, Secretary-General of the Association of Passenger Vehicles, analyzed, “The excellent performance in the first half of the year was firstly based on the abnormally low base of the same period last year; in addition, the rapid growth of the new energy market was another important driving force. In June, the sales trend of passenger cars It was slightly weaker than in previous years, mainly because of the imbalance of supply and demand caused by the shortage of global automotive chips; especially in June, the shortage of chips caused a sharp drop in domestic passenger car wholesale sales, which in turn affected retail sales."

From the perspective of production, from January to June, the cumulative domestic production of narrow passenger vehicles was 9.547 million, a year-on-year increase of 28.1%. However, the impact of "core shortage" has become more and more obvious. In June, the output of narrowly defined passenger vehicles has fallen by 13.9% year-on-year; among them, joint venture brands have fallen by 35%. In contrast, self-owned brands have effectively relieved the pressure of chip shortages by continuously strengthening their supply chain advantages and implementing more flexible measures to stabilize production and sales, and achieved a positive growth of 20% in June.

The overall obstruction of production has also led to the suppression of the wholesale end. From January to June, the manufacturer's cumulative wholesale volume was 9.817 million vehicles, a year-on-year increase of 28.0% and a decrease of 100,000 vehicles from the same period in 2019. Focusing on June, the manufacturer's wholesale volume dropped to 1.531 million vehicles across the board, down 4.9% month-on-month, down 10.2% year-on-year, and down 9% year-on-year.

Under the combined influence of multiple factors, manufacturers’ inventory continues to decline. As of the end of June, manufacturer inventory decreased by 20,000 units from the previous month, and channel inventory decreased by 160,000 units from the previous month. In the first half of the year, manufacturer inventories decreased by 230,000 units, which was significantly larger than the same period in the previous year. This has led to the phenomenon of product discounts and recovery in the terminal market.

In terms of vehicle types, from January to June, a total of 4.823 million sedans were sold, a year-on-year increase of 30.1%, leading the growth rate; a total of 563,000 MPVs were sold, a year-on-year increase of 30.0%, followed by a growth rate; and a total of SUVs were sold. 4.556 million vehicles, with a growth rate of 27.5%, were the slowest growth models in the first half of the year, and the sales gap between them and cars has also been widened.

Leading the car market is inseparable from the strong boost of the new energy market. From January to June, the wholesale and retail of new energy passenger vehicles exceeded one million; among them, the wholesale volume of new energy was 1.087 million, a year-on-year increase of 231.5%; the retail volume was 1.001 million, a year-on-year increase of 218.9%. The Passenger Association had predicted that the annual sales of new energy passenger vehicles would reach 2.4 million units, and judging from the current growth rate, it is clearly expected to surpass this goal.

It is worth noting that new energy vehicles are also a breakthrough in my country's auto export growth. In June, the export volume of new energy vehicles showed explosive growth. Among them, the export volume of Tesla China was 5,017, and the export volume of SAIC passenger car, BYD and JAC were 2,300, 215, and 127 respectively. Other car companies are also gaining momentum.

In terms of vehicle series, in June, although the enthusiasm for high-end cars declined slightly, it remained stable. A total of about 250,000 vehicles were sold, a year-on-year decrease of 1% and a month-on-month decrease of 4%; an increase of 28 compared to June 2019 %, the demand is still strong. Independent brands with a more complete domestic system and more flexible procurement methods stand out. In June, about 600,000 vehicles were sold, a year-on-year increase of 16% and a month-on-month increase of 2%; their retail share also increased by 7 percentage points to 38%. . In sharp contrast, in June, the retail volume of mainstream joint venture brands was approximately 730,000, a year-on-year decrease of 18%, a month-on-month decrease of 7%, and a decrease of 22% from June 2019; among them, the share of Japanese brands fell by 2.5 percentage points. To 23%, the American system slightly increased by 0.6 percentage points to 10.8%, while the German system is still accumulating power.

Looking forward to the second half of the year, the "passive" destocking characteristics of manufacturers due to chip shortages are expected to change. According to the analysis of the Federation of Travel Services, the problem of chip shortages is expected to be significantly eased in the third quarter, and the trend of manufacturers to replenish inventory will gradually appear. As a result, the wholesale market may pick up strongly from August.

Looking forward to July, there will be a total of 22 working days, with sufficient time for effective production and sales. At the same time, the production cut caused by the previous "core shortage" problem is expected to gradually improve; in addition, the demand for self-driving tours in the summer is also expected to increase further. The auto market is enthusiastic. However, July is also the off-season for sales over the years. The hot weather has reduced consumers’ enthusiasm for choosing and buying cars when they go out. Manufacturers’ high-temperature vacations are also concentrated in this period. Therefore, from a macro perspective, the short-term operating pressure of small and medium-sized enterprises will still exist, and the purchasing power of low- and middle-income groups will delay recovery, which will affect the growth of the auto market.

Notice on Holding the Rui'an Promotion Conference for the 2025 China (Rui'an) International Automobile and Motorcycle Parts Exhibition

On September 5th, we invite you to join us at the Wenzhou Auto Parts Exhibition on a journey to trace the origin of the Auto Parts City, as per the invitation from the purchaser!

Hot Booking | AAPEX 2024- Professional Exhibition Channel for Entering the North American Auto Parts Market

The wind is just right, Qianchuan Hui! Looking forward to working with you at the 2024 Wenzhou Auto Parts Exhibition and composing a new chapter!

Live up to Shaohua | Wenzhou Auto Parts Exhibition, these wonderful moments are worth remembering!

Bridgestone exits Russia and sells assets to S8 Capital

Free support line!

Email Support!

Working Days/Hours!

Copyright © 2018, PKT Auto Parts All Rights Reserved

浙ICP备18033565号-1

浙公网安备33038102332475号

浙公网安备33038102332475号

English

English Chinese

Chinese