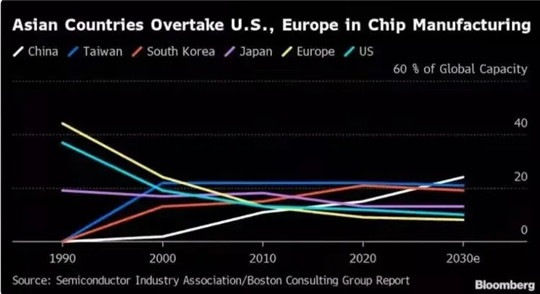

With the tide of core shortage sweeping the world, a new round of mergers and acquisitions has also been set off within the semiconductor industry, and a new pattern is quietly brewing.

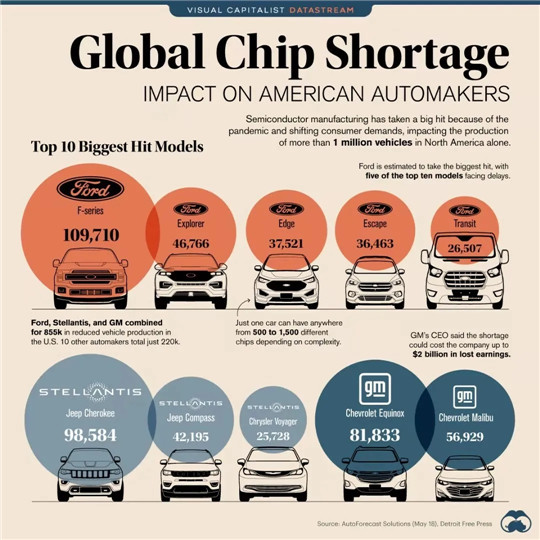

The sharp sharp knife that is short of chips is leaving dense scratches in more and more market areas. Even the smartphone industry, which has been able to "single its own body" before, has also begun to encounter a new round of capacity and delivery challenges under the shadow of the chip shortage.

For a long time in the past, smartphone manufacturers have been "watching the fire from the other side" in the crisis of chip supply. Seeing the anxiety of major car and home appliance players like ants on a hot pot, now, this fire is about to burn to their own homes. At the door. The slowdown in production, rising prices and the delayed launch of new products are all realistic portrayals of the current difficulties in chip supply in the mobile phone industry.

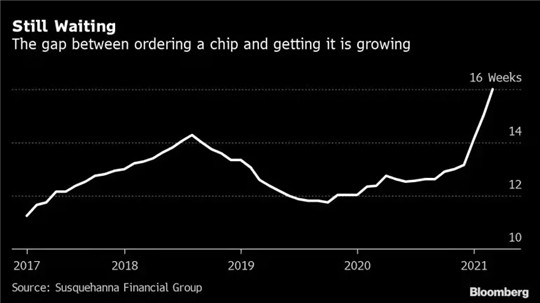

Although TSMC has given a forecast that "automobile chip problems may be alleviated in the third quarter," looking at more regions and industries around the world, the chip crisis is still in a state of raging.

Take the current smartphone industry that has just been involved in the lack of core vortex. In addition to the lack of 4G and 5G chipsets, manufacturers are also encountering difficult supply difficulties in display drivers, application processors and other semiconductor accessories. In the smart phone industry, 80% of manufacturers are falling into the predicament of chip shortages.

The chip layout has also ushered in a new reshuffle.

Also in the last six months, with the tide of core shortage sweeping the world, a new round of mergers and acquisitions has also been set off within the semiconductor industry, and a new pattern is quietly brewing.

Just recently, Nexperia intends to acquire NWF from the UK for 63 million pounds. This is the largest acquisition in the history of my country’s chip development. Don't think that China Chip Semiconductor can chant victory and set sail overseas. Because the scale of mergers and acquisitions in the United States is far greater than that in China.

Not long ago, Intel announced the acquisition of GlobalFoundries for US$30 billion. The 350-fold difference in the amount means that if China's chip semiconductor wants to narrow the gap with the world's advanced level through mergers and acquisitions, it is not easy at least for the moment-especially for the chip manufacturing industry that pays attention to scale and value chain.

The largest acquisition in my country's chip history

Wingtech made an announcement earlier this month that its wholly-owned subsidiary, Nexperia BV, will acquire NWF (Newport Wafer Fab), the largest chip manufacturer in the UK. After the transaction is completed, Nexperia will hold 100% of the latter. % Equity.

On July 5th, Anshi Semiconductor signed a related acquisition agreement with NWF parent company NEPTUNE 6 LIMITED and its shareholders. Although the official announcement did not disclose the final transaction amount, according to external news, Anshi Semiconductor may initiate this cross-border acquisition with 63 million pounds (approximately 564 million yuan).

It is worth mentioning that if the acquisition goes smoothly, this transaction will be the largest semiconductor acquisition in my country’s history, and it will also be the first time a Chinese chip manufacturer has acquired a world-leading, established foreign semiconductor company.

For many readers in China, Anshi Semiconductor may not be unfamiliar. The company's predecessor was the standard product business unit of Dutch semiconductor giant NXP (NXP Semiconductors N.V.,). It was formally separated from NXP in 2016 and was later acquired by China Wingtech Technology in 2019 and 100% controlled. Anshi Semiconductor is an IDM manufacturer, and its current business scope covers all aspects of semiconductor design, manufacturing, packaging and testing.

NWF is located in Newport, South Wales, UK. It is currently one of the few semiconductor chip manufacturers in the UK. Its core business is mainly to produce silicon chips for power applications for the automotive industry. As early as 2019, Anshi Semiconductor became the second largest shareholder by investing in its parent company Neptune 6 Limited. Later, it also has close business ties with NWF and is an important customer of the latter's foundry.

It is worth mentioning that NWF’s parent company NEPTUNE 6 is currently in a state of insolvency. In the past fiscal year 2020, the company’s total assets at the end of the year were 44,707,600 pounds, net assets were negative 5,177,300 pounds, and liabilities were close to 5,000. Ten thousand pounds. According to CNBC's news, NMF currently owes 20 million pounds to HSBC and 18 million pounds to the Welsh government. These debts will be transferred to Anshi Semiconductor for repayment in the future.

But in the view of Anshi Semiconductor, NWF is not a hot potato. At present, Nexperia's wafer factory does not have the production capacity of IGBT chips. The acquisition of NWF, in addition to expanding the existing capacity, is essentially an effective supplement to the shortcomings of the product line.

The significance of this acquisition lies in the layout of third-generation semiconductors. The industry generally believes that one of the most important reasons why Anshi Semiconductor has focused on NWF and included it under its command at a price of up to 63 million pounds is that the latter has third-generation semiconductors (mainly silicon carbide Sic and nitride Gallium GaN) research and development capabilities.

However, at a difficult time when the global chip shortage continues to brew, the most important semiconductor company in the UK is about to be sold to Chinese companies. This matter has also encountered the intervention of the British government in recent days.

British Prime Minister Johnson has made it clear that the British National Security Advisor will review the entire process of this acquisition. According to the relevant laws and regulations of the United Kingdom, the government has 30 days to decide whether to release a corporate acquisition or to review related acquisitions——

Once the government decides to initiate a review, the review process may take up to five years. If it is deemed threatening, the government has the right to finally cancel the transaction.

Intel pulls the sword

Also a week ago, the Wall Street Journal cited sources familiar with the matter as saying that Intel is considering the acquisition of semiconductor manufacturer GlobalFoundries Inc (GF, US foundry company GlobalFoundries) for $30 billion, but related progress is still in progress. Negotiation stage.

At a critical moment when the entire US auto industry continues to "core panic", the representative of Intel’s technology, Pat Gelsinger, who has been away from Intel for a decade, returned with a high profile at the beginning of this year to take over as the new CEO of Ruibo. . Shouting the reform slogans of "Intel is back" and "The old Intel is now the new Intel", Kissinger injected the dull Intel for a long time not only as a booster, but also as a sober agent.

This is a key turning point in Intel’s fifty-year history. In order to help the company recover the “missed ten years”, he is about to start a top-down “major operation” at the pinnacle of power to find new opportunities for the company. Strategic Direction. One of the decisions for transformation is the new IDM 2.0 strategy, which is to restart the foundry business on the premise of stabilizing the basic disk of the IDM model.

Obviously, if Intel wants to expand in the field of foundry business in the future, then the significance of the acquisition of GlobalFoundries is very important. The most direct benefit is to help Intel to further increase chip production capacity.

Currently, GlobalFoundries is headquartered in the United States and is controlled by Mubadala Investment, an investment agency of the Abu Dhabi government. According to relevant data from the research organization TrendForce, GlobalFoundries' total revenue in 2020 will account for approximately 7% of the chip foundry industry, which is second only to the industry leaders TSMC and Samsung, and is basically the same as the third-ranked UMC. .

In view of the high proportion of GlobalFoundries in the field of chip foundry, once the company is acquired by Intel, this will have a far-reaching impact on the pattern and direction of the entire semiconductor chip industry.

Just in June of this year, Reuters also broke Mubadala's intention to IPO GlobalFoundries, but as of now, the company has not commented on Intel's acquisition negotiations.

As early as 2008, Intel and AMD chose two completely different development paths. The former continued to manufacture its own chips to maintain a high degree of control, while AMD decided to split its semiconductor business into GlobalFoundries, relying on Global Fangde and other companies jointly grab the foundry market.

According to the external news, the news that Intel intends to acquire GlobalFoundries is not groundless, because the company has been promoting the new process of foundry on multiple fronts since the launch of the New Deal, and it has come from the process technology focused by the two companies. Look, the two sides also have complementary business advantages.

Of course, this acquisition also has real considerations of geo-economics.

Continued lack of cores, the United States panicked. The Biden administration is working to resolve the chip supply chain crisis. In order to solve the impact of chip shortages on the automotive industry, the United States has prepared legislation to promote semiconductor production and supply. At an extraordinary time, Intel, as the US chip dominator, has an unshirkable responsibility. Its new head promulgated a series of new policies and a series of actions. Naturally, it must also conform to the United States' short- to medium-term national will.

Once Intel’s acquisition of GlobalFoundries is firmly established, this will undoubtedly be a business and strategic threat to TSMC and Samsung, who are hesitant to go to the United States to build a large-scale factory.

A new wave of acquisitions and integrations is set off globally

Actually, Nexperia's acquisition of semiconductors is blocked, which is not an exception in the world. In the critical year of global chip shortage, more and more countries are cautious about the acquisition of semiconductors by overseas companies.

In May of this year, Magna chip (Magnachip) was sold to China's Wise Road Fund (Wise Road), it was scrutinized by South Korean regulators on the grounds that it involved "core technology at the national level," and the U.S. Treasury Department also required All parties involved in the transaction submitted relevant transaction documents to the U.S. Transnational Investment Commission in an attempt to block the $1.4 billion acquisition.

The timeline is pushed forward. In March of this year, the Italian government used "strategicly important industries" as an excuse to prevent China Shenzhen Investment Holdings from acquiring the Milan-based semiconductor company LPE.

Since AMD announced last year that it plans to acquire Xilinx for 35 billion U.S. dollars, and was approved by the shareholders of both parties in April this year, its subsequent acquisition plan has also been investigated by British regulators and the European Union.

Despite this, under the weight of the "core panic", more and more chip manufacturers are starting to race their tracks, seeking to expand their scale and broaden their product portfolios on a global scale. In the past year, a wave of mergers and acquisitions has swept the semiconductor industry.

In July last year, the chip giant Analog Devices Inc (hereinafter referred to as ADI) planned to acquire rival Maxim Integrated, becoming one of the largest chip acquisitions in the industry in 2020.

Also in the second half of last year, Nvidia announced that it had reached an agreement with Japan’s Softbank to acquire the chip architecture company ARM from the latter for US$40 billion, which caused a huge sensation in the industry. As soon as the news came out, Qualcomm, Apple and other companies expressed resistance to the merger. After all, ARM's chip design architecture monopolizes more than 95% of mobile chips. At this stage, even Huawei and Xiaomi phones use ARM architecture.

This also means that once Nvidia successfully acquires ARM, the above-mentioned technology companies must obtain consent from Nvidia if they want to continue to use ARM's architecture design chips. In order not to be "stuck" by Nvidia, more and more companies have chosen to stand up and boycott it. Even the regulatory agencies of the United Kingdom, China, and the United States have successively launched antitrust investigations and said "no" to this merger and acquisition.

The more the chip shortage, the more people worry about the formation of a new monopoly, but this does not affect the intensification of industry consolidation and mergers and acquisitions.

According to incomplete statistics from "Auto Commune" and "C Dimension", since the second half of 2020, the global mergers and acquisitions of large-scale chips have exceeded 120 billion U.S. dollars, a record high in just one year. Among them, half of the transactions are closely related to the automotive industry.

As the master of systems science Denera Meadows wrote, diversified systems with more access and redundancy tend to be more robust than singular systems with few differences when they are impacted or affected by external forces.

Faced with the most severe "feedback delay" of chip supply shortage, more and more semiconductor companies have realized that only in the process of expansion and subversion can they not be left behind in the tide of the times. The large-scale mergers and acquisitions within the industry are the key to the self-subversion of enterprises and a precursor to the reshaping of the industry.

Of course, TSMC Wei Zhe’s family should not be full of pretty words. On the one hand, even if TSMC, which is at the top of the industry, has increased the output of its own factories, it is difficult to directly influence the supply of the entire industry on its own. On the other hand, let's talk about the long-arm jurisdiction of the United States as air.

Notice on Holding the Rui'an Promotion Conference for the 2025 China (Rui'an) International Automobile and Motorcycle Parts Exhibition

On September 5th, we invite you to join us at the Wenzhou Auto Parts Exhibition on a journey to trace the origin of the Auto Parts City, as per the invitation from the purchaser!

Hot Booking | AAPEX 2024- Professional Exhibition Channel for Entering the North American Auto Parts Market

The wind is just right, Qianchuan Hui! Looking forward to working with you at the 2024 Wenzhou Auto Parts Exhibition and composing a new chapter!

Live up to Shaohua | Wenzhou Auto Parts Exhibition, these wonderful moments are worth remembering!

Bridgestone exits Russia and sells assets to S8 Capital

Free support line!

Email Support!

Working Days/Hours!

Copyright © 2018, PKT Auto Parts All Rights Reserved

浙ICP备18033565号-1

浙公网安备33038102332475号

浙公网安备33038102332475号

English

English Chinese

Chinese