A few days ago, the Passenger Association announced the wholesale sales of passenger cars in a narrow sense in July. The sales data shows that the wholesale sales of passenger vehicles in the narrow sense in July was 1.507 million, a year-on-year decrease of 8.7% and a decrease of 1% from the same period in 2019. According to the analysis of the Travel Association, the wholesale sales of passenger cars in the narrow sense have declined in recent months, which is still caused by the widespread shortage of chips in the industry. However, due to the strong resilience of the industry chain, the leading auto companies can effectively resolve the pressure brought about by the shortage of chips, turning disadvantages into advantages, and have achieved significant growth. However, the supply gap of joint venture brand parts is relatively large, and the overall market share has declined. .

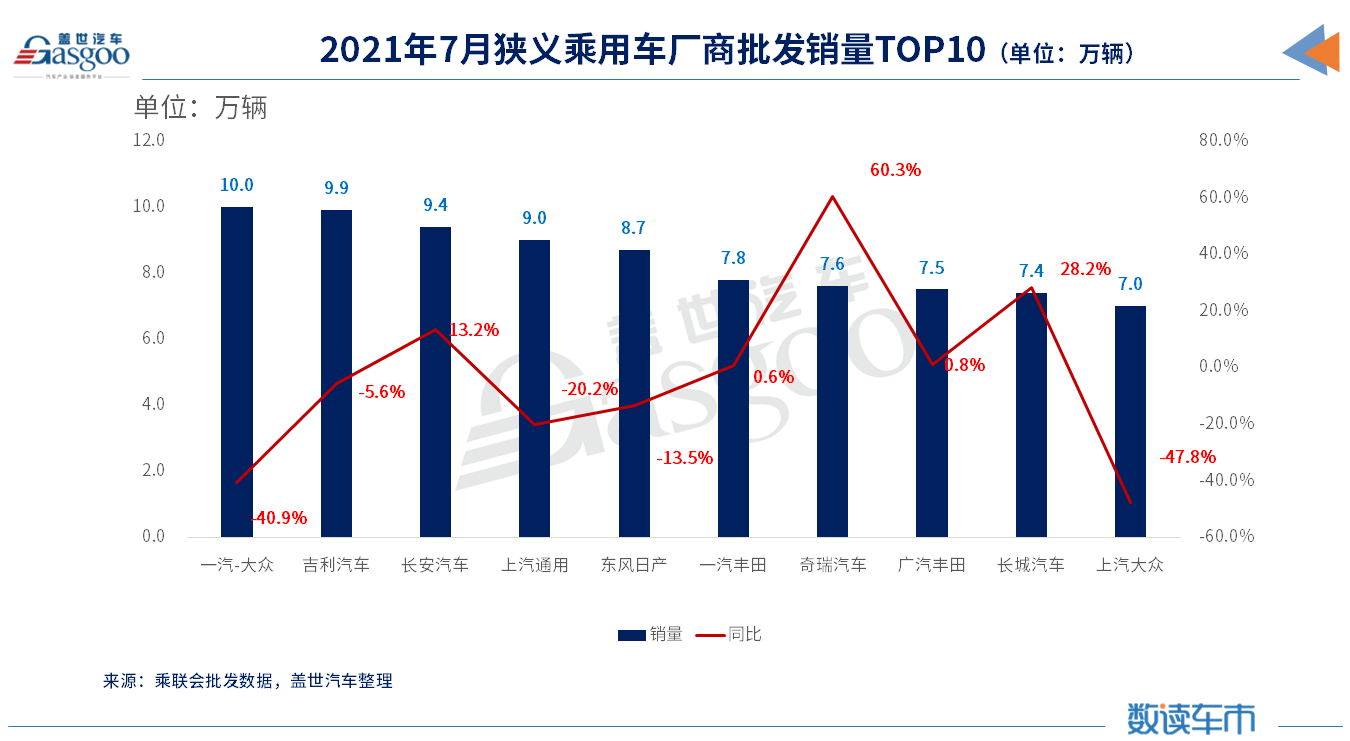

Under the new situation of chip shortages, the wholesale sales rankings of narrow passenger car manufacturers have also seen new changes compared with the past. The TOP 10 car companies in narrow passenger car manufacturers wholesale sales in July showed the following two major trends: 1. Independent car companies The overall strength is strong, with leading auto companies such as Geely and Changan both entering the top three; second, the overall decline of mainstream joint venture car companies, German and Japanese companies are facing certain pressure.

Strengthen independently: Geely and Chang'an are among the top three finalists

In the context of chip shortage, leading auto companies with independent brands have ushered in a strong momentum of development. Geely and Changan both entered the top three in the TOP 10 wholesale sales of passenger car manufacturers in the narrow sense in July, ranking second and third respectively.

Geely Automobile sold 99,000 units in July, which is a small gap compared with the first-ranked FAW-Volkswagen’s monthly sales of 100,000 units. The reason why Geely can compete with FAW-Volkswagen in terms of size is not only that its original star models such as Boyue and Emgrand can continue to sell well, but also that the CMA high-end series "China Star" has gradually grown into the main sales force. The data shows that the sales of the three models of Xingrui, Xingyue S, and Xingyue L were 18,000 in July, showing the momentum of hot sales. It has not been fully released, so the next "Star Series" will have more room for growth. In addition, Lynk&Co and Geometry have achieved varying degrees of sales growth in July, which also contributed to Geely's increase in sales.

Geely brand CMA high-end series "China Star"; Source: Geely Automobile

Changan Automobile has been developing rapidly this year, and has repeatedly squeezed into the top three in the narrow sense of passenger car sales per month. In July, Changan Automobile sold 94,000 vehicles in a single month, an increase of 13.2% year-on-year. Most of this sales volume is contributed by CS75 series and Yidong series. According to official data provided by Changan Automobile, the CS75 series has exceeded 20,000 units for 16 consecutive months, while the Yidong series is now basically stable at more than 10,000 units. In addition, with the enrichment of its products, the UNI series has become Changan's third main vehicle series after the CS75 series and the Yidong series. It is reported that with the hot sales of the UNI series, Changan may independently become a high-end brand. Although this matter has not received a clear response from Changan Automobile, the industry believes that under the background of the general "high" of independent brands, Changan It is only a matter of time for the UNI series to go from high-end product sequence to high-end brand.

In addition to Geely and Changan, the other two independent brands that were shortlisted for July's narrow passenger car manufacturers' wholesale sales TOP 10 are Chery and Great Wall respectively. What is worthy of recognition is that Chery Automobile's sales in July reached 76,000, an increase of 60.3% year-on-year. In July, its ranking in narrow passenger car manufacturers' wholesale sales also rose from ninth in June to seventh.

Chery Automobile sales have risen again, which is still the result of multi-brand operations. Among them, among Chery brand passenger cars, Tiggo 8 is the absolute sales leader, followed by Arrizo 5. Chery's Jietu formally became a brand independent from the previous product series. Now Jietu's two major product series Jietu X70 and Jietu X90 are the main sales contributors, and the combined monthly sales of the two series products have basically stabilized at more than 10,000 units. However, Xingtu, as a high-end brand of Chery, has a mediocre market performance. However, Chery New Energy’s sales this year has risen sharply. Data shows that from January to July this year, Chery’s cumulative sales of new energy products were 48,000, a year-on-year increase of 212.5%.

Chery Little Ant has sold 30,674 units in the first half of the year, an increase of 215.2%; Source: Chery Automobile

Great Wall Motor’s passenger vehicle sales reached 74,000 in July, a year-on-year increase of 28.2%. Today, in addition to Great Wall pickups, Great Wall has four major brands that focus on the passenger car field, namely Haval, WEY, Euler, and Tanks. In July, Haval brand sales were 57,000 units, a year-on-year increase of 20.4%, of which Haval H6 contributed 26,000 units. Although the status of Haval H6 is still the backbone of the Haval brand system, the addition of Haval Big Dog, Haval Red Rabbit, Haval First Love and other products greatly broadens the product boundary of Haval SUV and brings more personalized choices to users.

Joint ventures go down: the Japanese are cautious, the Germans are worried

In July, the sales of joint venture auto companies fell again. Judging from the car companies that were shortlisted for the TOP 10 in narrow passenger car manufacturers' wholesale sales volume in July, the sales of North and South Volkswagen both saw a large decline in July, and the gap in volume between the two is still large. Among them, FAW-Volkswagen sold 100,000 vehicles in July, down 40.9% year-on-year; SAIC-Volkswagen sold 70,000 vehicles in July, down 47.8% year-on-year. Industry insiders pointed out that the fundamental reason for the widening gap between North and South Volkswagen is that FAW-Volkswagen has “backed” by Audi, because luxury brands still have strong market potential under the consumption upgrade trend. In addition, in the entry-level market, Jetta's performance is obvious Better than Skoda, the superposition of these two factors makes FAW-Volkswagen's overall performance better than SAIC-Volkswagen.

In fact, for Volkswagen brands, electrification is undoubtedly its main direction in the future. At this stage, both the North and South Volkswagen have introduced ID. series models, but the user acceptance of these products in the Chinese market is not high. For example, ID.4 X and ID.4 CROZZ, which were introduced to the Chinese market earlier, have the highest monthly sales volume of only 2000. More than one. Next, how to increase the market share of electric vehicles in China is a difficult problem for the public.

ID.4 series of two models; source: Volkswagen

In addition to the continuous "downhill" of the North and South Volkswagen, the Japanese market, which has always been stable, is now starting to "stall" in the context of a shortage of chips. In July, Dongfeng Nissan sold 87,000 vehicles, down 13.5% year-on-year. Today, Sylphy is still carrying the banner of Dongfeng Nissan's sales. With monthly sales of over 40,000, Sylphy has become the envy of many competitors, but for Dongfeng Nissan, there is also the risk of "it is hard to grow a single tree." In July, Dongfeng Nissan launched a new generation of Qijun. This model can be regarded as a blockbuster product that Dongfeng Nissan put on the market this year. Naturally, it also has a lot of hope. However, because the new generation of Qijun is equipped with a three-cylinder engine, Therefore, the industry is not very optimistic about its future performance.

Under a series of uncertain factors such as core shortage and epidemic situation, Toyota, which has always been cautious, adopted a conservative strategy of step by step at this time. Under this strategy, both North and South Toyota achieved positive growth in July, which can be called a "warm current" among joint venture brands whose main theme is decline. This year, despite the many threats to the market environment, Toyota has launched a product offensive in the Chinese market. Products such as Asia Lion, RAV4 Rongfang Double Engine E+, and the new fourth-generation Highlander are advancing steadily, and the crown has become independent. Crown Lufang, which will be launched soon after the brand, will help Toyota strengthen its competitiveness in different market segments, thereby further increasing its market share in China.

This article is reproduced from Gasgoo.com

Notice on Holding the Rui'an Promotion Conference for the 2025 China (Rui'an) International Automobile and Motorcycle Parts Exhibition

On September 5th, we invite you to join us at the Wenzhou Auto Parts Exhibition on a journey to trace the origin of the Auto Parts City, as per the invitation from the purchaser!

Hot Booking | AAPEX 2024- Professional Exhibition Channel for Entering the North American Auto Parts Market

The wind is just right, Qianchuan Hui! Looking forward to working with you at the 2024 Wenzhou Auto Parts Exhibition and composing a new chapter!

Live up to Shaohua | Wenzhou Auto Parts Exhibition, these wonderful moments are worth remembering!

Bridgestone exits Russia and sells assets to S8 Capital

Free support line!

Email Support!

Working Days/Hours!

Copyright © 2018, PKT Auto Parts All Rights Reserved

浙ICP备18033565号-1

浙公网安备33038102332475号

浙公网安备33038102332475号

English

English Chinese

Chinese